Taxation of condo associations is an area with a lot of confusion. Many associations believe they are tax-exempt as “non-profits” and are not required to file a condo association tax return.

As a CPA firm that files condo tax returns for clients in all 50 states, we have heard this argument often. Unfortunately, it is just not correct. Condo associations have certain tax filing requirements that are specific to them.

Easy Links- Do condo associations have to file tax returns?

- Condo Association Tax Filing Options

- Condo Association Filing Requirements

- Condo association tax return: What about non-exempt activities?

- Form 1120-H Advantages and Disadvantages

- Key Components of the Condo Association Tax Return

- Top Section

- Income and Expenditures

- Gross Income

- Deductions

- Tax Liability/Payment

- Signature

- Filing the Condo Association Return

- We serve condo associations in all 50 states

Do condo associations have to file tax returns?

Condominium associations are entities that enforce rules and guidelines regarding the community management. They are required to file federal tax returns.

Most states (that have an income tax) follow the federal guidelines. However, filing requirements and tax rates will vary state by state.

Even though a tax return is required, this does not mean that the condo association will owe any tax. Most activities of the association will be considered exempt income (more about this later).

Condo Association Tax Filing Options

Before a condo association files a tax return it will need to examine the two available options: (1) Form 1120-H; and (2) Form 1120.

In this post, we’re going to examine how condo associations are taxed and focus on the different sections of Form 1120-H. This form was designed specifically for HOAs and condo associations.

But in some situations it may make sense for an association to file Form 1120. We have taken a close look at the form differences here.

Condo Association Filing Requirements

IRS code section 528 spells out the filing requirements for qualifying condo associations. Assuming an association qualifies, it will not have to pay tax on any net profit as long as that profit relates to “exempt activities.”

Specifically, they can exclude “exempt function income” from gross income. This results in the association being able to show a lower taxable income.

Exempt activities are activities that relate to general membership functions. Condominium associations collect dues from members. These then go towards the management and other services relating to the property. This includes landscaping, building maintenance, garbage, etc.

In addition, a condo association generally owns the building structures. Accordingly, and it is responsible for common upkeep like roof repairs and other building maintenance.

Membership dues and assessments would represent exempt income. Likewise, funds that are used for the maintenance and upkeep of the association property would be defined as exempt expenses.

Condo association tax return: What about non-exempt activities?

A condo association may though have “non-exempt activities.” These relate to any activities that are not in the normal course of activities or represent a commercial gain. This could be laundry income and also other items like dividends, interest, sales of stocks, rental income, royalties, etc.

In order for a homeowners association to take advantage of these tax benefits, the association must elect to do so under section 528 by filing Form 1120-H. The association must make this election each tax year by the due date of the return (including extensions).

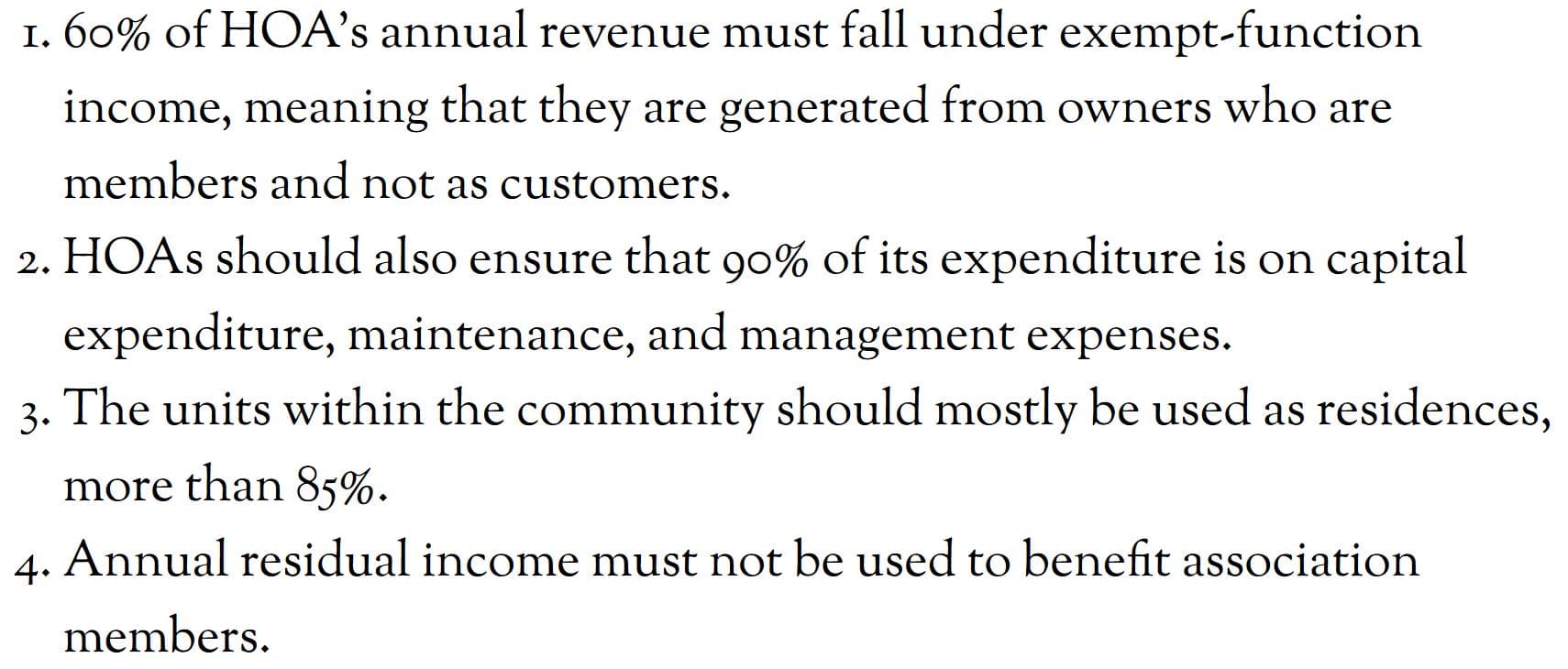

So what are the section 528 requirements? Before we examine the specific parts of form 1120-H, let’s take a look at the filing requirements. There are four main qualifications to file the return:

Form 1120-H Advantages and Disadvantages

There are many advantages to Form 1120-H including the following: (1) it is a somewhat simple one-page form; (2) there is no need to prepare or file a balance sheet; (3) the association does not need to make any estimated tax payments; and (4) a standard deduction of $100 is allowed for any condo association tax return.

But there are a few disadvantages of the 1120-H like: (1) any net non-exempt income is taxed at a flat 30% rate instead of standard corporate tax rates; (2) there are specific rules regarding expenditure allocations; (3) there is no net operating loss carryover; and (4) there are no special deductions or exemptions like those available to many regular corporations.

Most condo associations have little or no net income attributed to exempt activities. But don’t forget that form Form 1120 has lower graduated tax rates. As such, it can make sense to file this return if the association has a large amount of non-exempt income, like mineral rights royalties. If the association generates substantial net exempt function income, then filing form Form 1120-H may make the most sense.

Key Components of the Condo Association Tax Return

So now that we understand what form to file, let’s take a closer look at the sections along with some of the filing issues.

As discussed, Form 1120-H allows the association to exclude exempt function income from the gross income. The main form components include the gross income, deductions and total tax and payments sections.

Top Section

Take a look above. Starting at the top, you’ll be asked to enter the basic information regarding the association.

In this section, you’ll you have to of course enter in your EIN (tax identification number) in addition to other basic information like association name and address. If this is a first year filing the HOA CPA may have the EIN.

Income and Expenditures

Next up, we launch straight into the finances and you’ll see four simple lines with blanks spaces at the end for your input; exempt functional income, total expenditures on the HOA, total other expenditures, and tax-exempt interest.

- Total Exempt Function Income: Annually or monthly dues & fees for membership. This relates only the members of the association and not any income relating to non-exempt activities.

- Total Association Expenditures: This is the expenditures made for maintaining and managing the association. At least 90% of the total expenditures must be made directly for the association.

- Total Other Expenditures: These are all the expenses that have no connection at all to the exempt function income.

- Tax Exempt Income: This is any income that isn’t taxed by the federal government (interest from bonds, for example).

Gross Income

The next section above relates to gross income from non-exempt activities. This includes dividends, taxable interest, gross rents, gross royalties, capital gain net income, net gain or (loss) from form 4797, and other income.

Deductions

The next section relates to deductions that relate to non-exempt income. If there is gross income in the previous section, you will enter any deductions in this section. Deductions include salaries and wages, repairs and maintenance, rents, taxes and licenses, interest, depreciation, and other related deductions.

Keep in mind this section refers to deductions connected to the production of gross income, excluding exempt function income.

Tax Liability/Payment

In this section, you’ll finish off by entering the totals including income and the amount you expect to pay (considering the 30% tax rate with Form 1120-H). Generally, the 30% tax rate will apply across the board which includes ordinary income and capital gains. Additionally, you won’t be able to carry forward a net operating loss as you would with Form 1120.

Signature

As with any IRS form, you will need to sign. The signature must be by the President of the HOA or any other authorized officer including the controller, treasurer, or chief accounting officer.

The ‘Paid Preparer’ section should remain blank if the form was self prepared. If you used a professional, like a CPA, they should fill out this section.

Filing the Condo Association Return

The association cannot revoke its election for that tax year unless the IRS consents. The association may request IRS consent by filing a ruling request along with a user fee.

We understand that associations can still be confused. Although it has only 1 page, you may spend hours trying to properly complete the form. A qualified accountant can save you a lot of time.

Completing a condo association tax return may sound easy. Many factors need to be considered and a DIY approach is not recommended. Make sure you are well versed on the tax code and hire a CPA if the process become too complex.

We serve condo associations in all 50 states:

Alabama, Alaska, Arizona, Arkansas, California, Colorado, Connecticut, Delaware, Florida, Georgia, Hawaii, Idaho, Illinois, Indiana, Iowa, Kansas, Kentucky, Louisiana, Maine, Maryland, Massachusetts, Michigan, Minnesota, Mississippi, Missouri, Montana, Nebraska, Nevada, New Hampshire, New Jersey, New Mexico, New York, North Carolina, North Dakota, Ohio, Oklahoma, Oregon, Pennsylvania, Rhode Island, South Carolina, South Dakota, Tennessee, Texas, Utah, Vermont, Virginia, Washington, West Virginia, Wisconsin, Wyoming